U.S. Hotel Performance Q3 2025

- Posted by admin

- On January 8, 2026

- 0 Comments

U.S. hotel performance in Q3 2025 showed steadiness with a mild late-summer dip. Room rates remained firm, supported by continued pricing discipline, steady corporate travel, and higher costs that encouraged hotels to maintain rate integrity. Revenue performance held up well, helped by strong demand during key summer weekends, regional festivals, and sporting events that boosted short bursts of occupancy. The early-September slowdown reflects the typical post-Labor Day pause and reduced weekend leisure travel. Performance strengthened again toward the end of the quarter as fall convention calendars resumed, including trade shows, corporate meetings, university events, and citywide conferences that lifted group and corporate demand. Major cultural events, late-summer concerts, and destination-specific festivals further supported demand patterns, helping hotels regain momentum despite normal seasonal softness in mid-quarter.

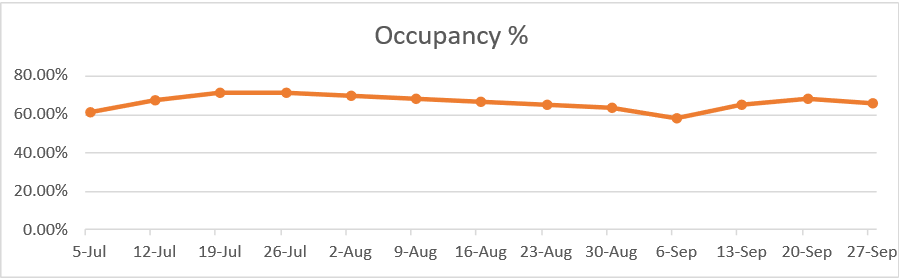

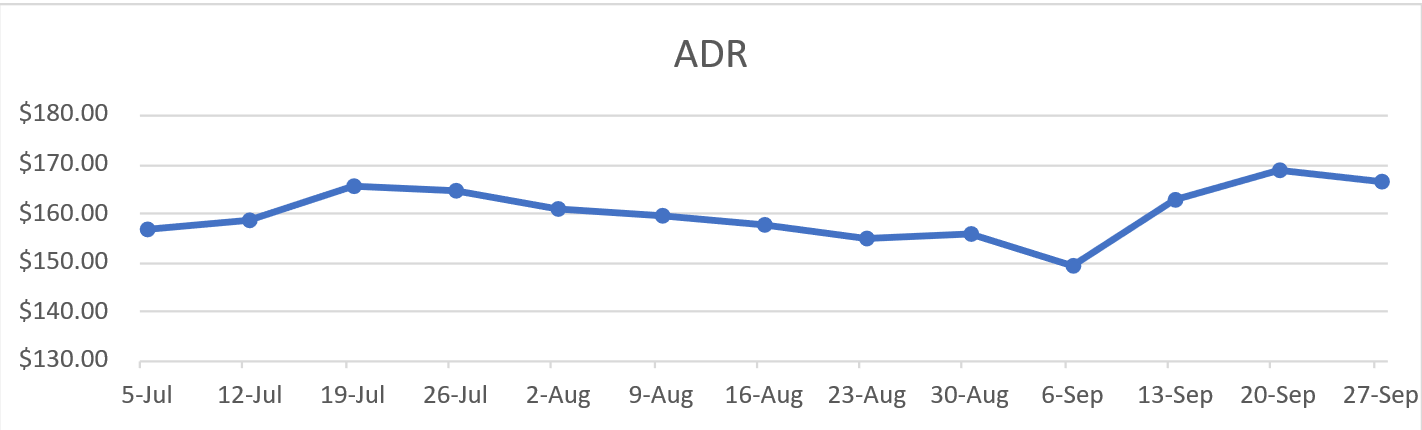

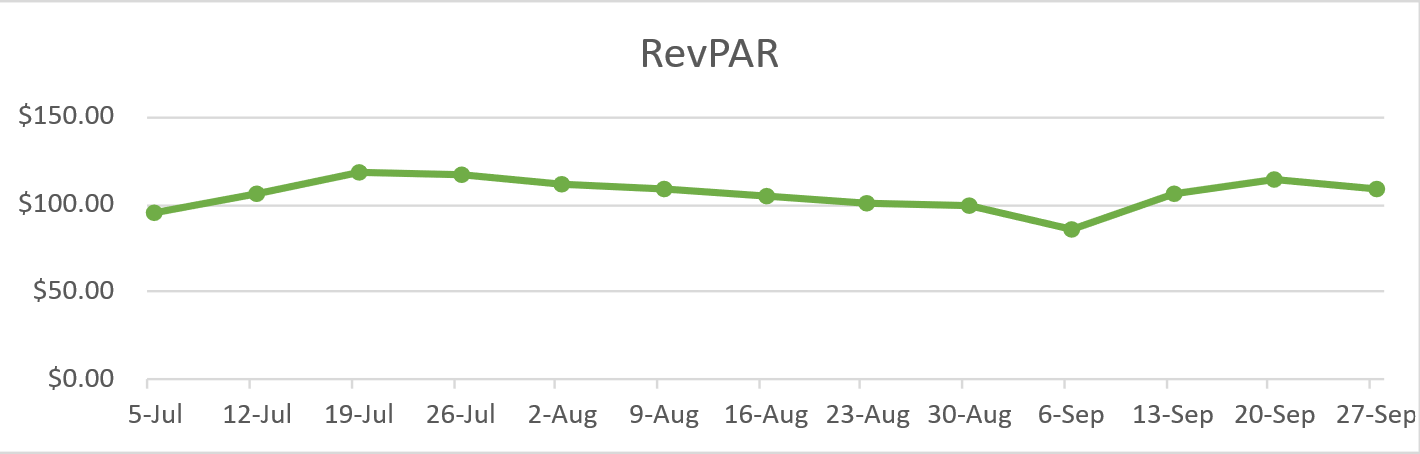

Occupancy was reported at 61.10% at the start of Q3 2025, which increased to 65.60% at the end of Q3 2025. ADR was $156.71 at the start of Q3 2025 which increased to $166.48 at the end of Q3 2025. RevPAR was $95.80 at the start of Q3 2025 which increased to $109.15 at the end of Q3 2025.

(Source: STR)

Analytical Summary

Major Q2 2025 transactions (By Sale Price)

| Hotel Name: EAST Miami

Location: Miami, FL No. of rooms: 352 Sale Price: $300,000,000 Price per unit: 852,273 per unit Seller: Certares Buyer: BRE Hotels & Resorts LLC |

|

| Hotel Name: Motto by Hilton New York City Chelsea

Location: New York City, NY No. of rooms: 374 Sale Price: $222,200,000 Price per unit: 594,118 per unit Seller: Magna Hospitality Buyer: Large institutional owners (undisclosed) |

|

| Hotel Name: The Westin Hilton Head Island Resort & Spa

Location: Hilton Head Island, SC No. of rooms: 420 Sale Price: $199,800,000 Price per unit: $475,714 per unit Seller: Southwest Value Partners Buyer: KSL Capital Partners |

|

| Hotel Name: Washington Marriott at Metro Center

Location: Washington, DC No. of rooms: 459 Sale Price: $177,000,000 Price per unit: $385,621 per unit Seller: Host Hotels & Resorts, Inc. Buyer: T2 Hospitality |

|

Source: CoStar

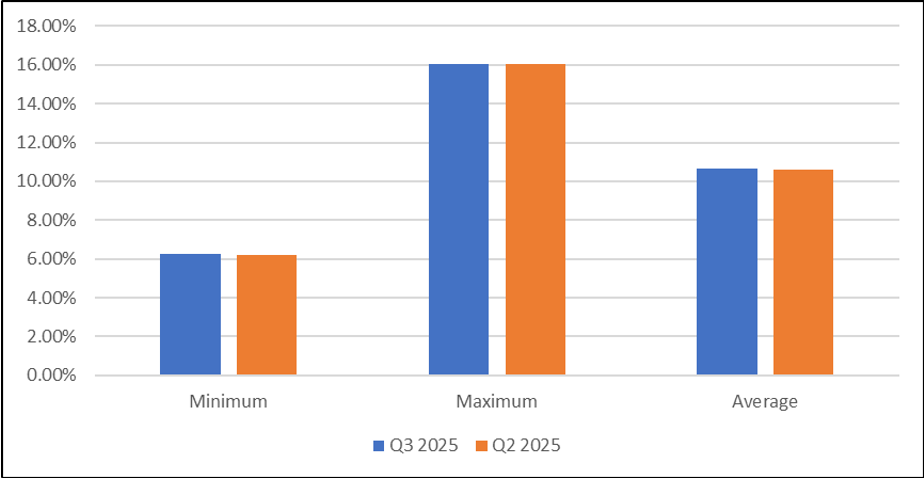

Q3 2025 Cap Rates

Average cap rates for U.S. hotels increased by 6 basis points in Q3 2025 as compared to Q2 2025. The following table illustrates minimum, maximum and average cap rates for U.S. hotels in Q3 2025 & Q2 2025.

(Source: RealtyRates.com)

| Cap Rate | Q3 2025 | Q2 2024 | Difference (bps) |

| Minimum | 6.27% | 6.18% | 9 |

| Maximum | 16.06% | 16.06% | 0 |

| Average | 10.68% | 10.62% | 6 |

Source: RealtyRates.com

Outlook

The U.S. hotel market is expected to enter Q4 2025 with flat RevPAR growth, reflecting a cooling travel environment. Industry forecasts from CBRE, STR, and CoStar indicate that demand softness and limited pricing power will continue into the final quarter of the year. Occupancy levels are projected to hover around 65%, which is low by historical norms and signals sluggish leisure and business travel. ADR gains are expected to be modest as hotels face resistance from price-sensitive consumers. Operating costs, particularly labor, insurance, and utilities, are likely to remain elevated, squeezing margins even if revenue holds steady. Luxury and upper-upscale hotels should outperform the broader market due to stronger high-income demand and better ability to raise rates. In contrast, economy and midscale hotels may see more pressure as competition from short-term rentals continues to siphon price-sensitive guests. The macroeconomic backdrop—characterized by sticky inflation, high interest rates, and geopolitical uncertainty—will likely keep travel sentiment cautious. Group and corporate travel may provide pockets of demand, but not enough to drive a broad-based surge. Supply growth in some metros could add further occupancy pressure, especially where new hotels are opening into a slow market. On the upside, any improvement in consumer confidence or international inbound travel could support a stronger Q4 than expected. Overall, Q4 2025 is shaping up to be a muted, margin-focused quarter, favoring operators with strong cost control and premium positioning.

0 Comments